April Monthly Insight

A bullish month across UK gas & power markets as gas storage concerns mount amid cooler weather.

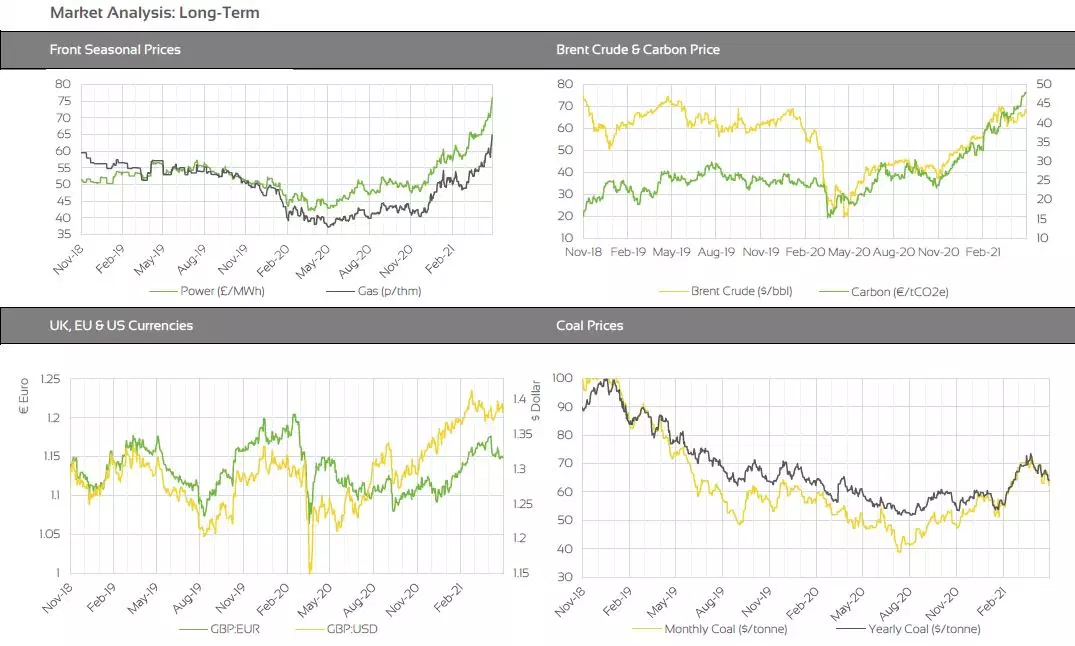

Market Insight - Long-Term

As with the front of the curve, movement on seasonal contracts has been extremely bullish throughout April. Much of the increase can be attributed to carbon prices, which have increased by over 12% through April. Whilst the commodity has been gaining momentum since Q3-21, on the back of increased investor interest, the EU’s decision to write increased emissions cut targets into policy, coupled with the US/China climate pledge, saw carbon prices hit new highs in April. Carbon prices feed into gas and power curves as generators using fossil fuels must purchase carbon permits to offset their emissions. Coal generation requires more permits to offset carbon, and so if the carbon price is rising, generators will fuel-switch and gas demand will increase, thus increasing gas prices too.

Oil prices have also risen this month, but gains have been kept in check by rising virus cases in some parts of the world. OPEC+ decided to proceed with planned output increases for May, during their April meeting this week. The market saw this as a vote of confidence from OPEC+ around global demand recovery. Favourable reports from China, on its oil demand and manufacturing output, have also supported prices.

Market Outlook

The short-term outlook is bullish with the potential for a little relief if temperatures and wind output improve as expected, after the first week of May. Storage fullness is the key concern and until the market starts to see storage injection overtake withdrawal, we are likely to see premiums remaining in prompt to near curve contracts. Further ahead, the outlook for front seasonal contracts remains bullish as we race to top storage up for winter. Contracts further ahead will be more led by carbon and oil. Whilst oil prices may begin to flatten, on rising Indian virus cases, carbon is showing no sign of giving recent gains back. Continued investor interest, and ever tougher climate targets, will continue to provide support.

Backwardation is still in full play across gas and power markets. Fixed clients with October 2021 renewals should look to conduct first rounds for renewals in the coming weeks to be fully prepared to act over the summer months. Alternatively, clients should select a longer-term flexible strategy to take advantage of any emerging opportunities to secure volume further ahead.

Download the full insight here:

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.