Energy Market Insight | August 2022

Gas & Power markets continued to remain volatile throughout August

Key Market Drivers

- Nord Stream 1 flows reduced to zero

- European storage levels hit 1st November target of at least 80% full

- Injections into Rough storage to re-commence early September

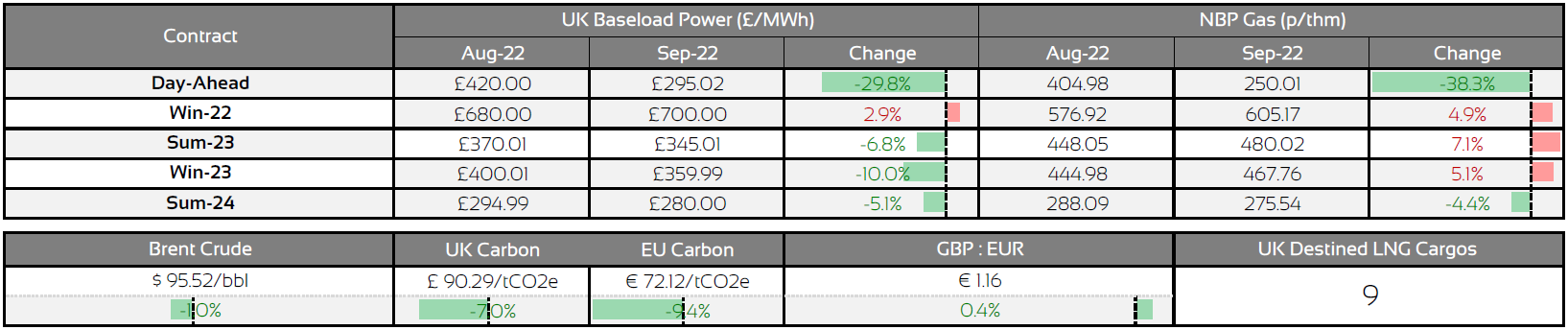

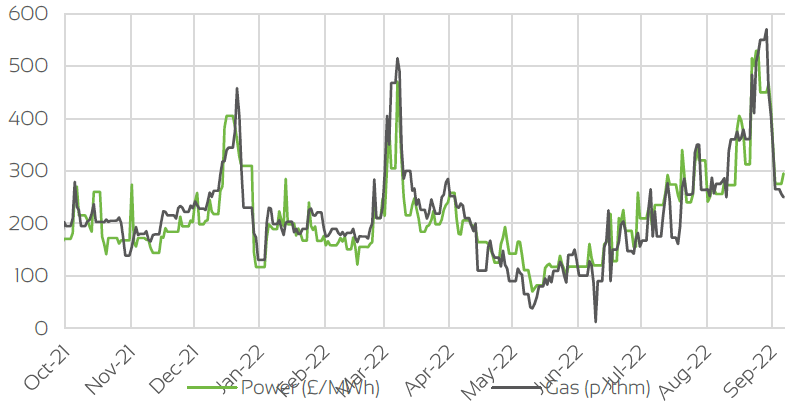

Day Ahead Prices

UK Temperatures

UK Demand

UK Supply Mix

Market Insight: Short-Term

Market volatility continued throughout August, as supply concerns persisted throughout the majority of the month, for both short term and longer term, contracts. Restricted gas flows from Russia, via both Nord Stream 1 and the Velke Kapusany pipeline through Ukraine remained throughout, with Nord Stream 1 going completely offline at the end of the month. In addition to this, global LNG supply continued to remain tight, with the re-opening of the Freeport LNG facility at about 80% capacity pushed back to the end of November and will not be back at full capacity until March.

Additionally, output in Australia, Peru & Egypt continued to be reduced only contributing to the tight global supply outlook.As we neared the end of the month, we did start to see prompt contracts lose considerable value as supply outlook started to look much more comfortable. Japan agreed a new deal with the new Sakhalin LNG project in Eastern Russia, reducing their reliance on LNG from other sources, alleviating some pressure.

In addition, LNG arrivals to the UK & North West Europe were strong with a new LNG pipeline due to open in the Netherlands, increasing European LNG capacity. The EU also announced that overall storage levels hit their 1st November target of at least 80% full, two months early, following a sustained period of strong injections. Injections are expected to continue, however, the EU believe this level provides them with a sufficient amount of gas in the system for this Winter.

The EU also announced that they are considering introducing a price cap on wholesale prices. Further details will be released by the EU commission on 14th September, but any introduction of a price cap is likely to weigh on prices. Additionally, Centrica have also confirmed that injections into Rough storage will re-commence early September.

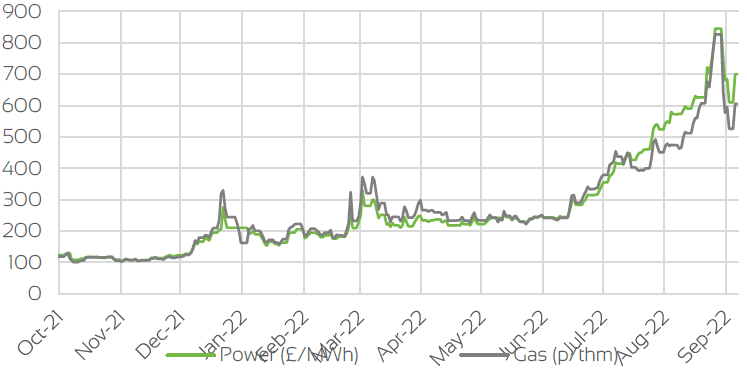

Front Seasonal Prices

Brent Crude & Carbon Price

UK, EU & US Currencies

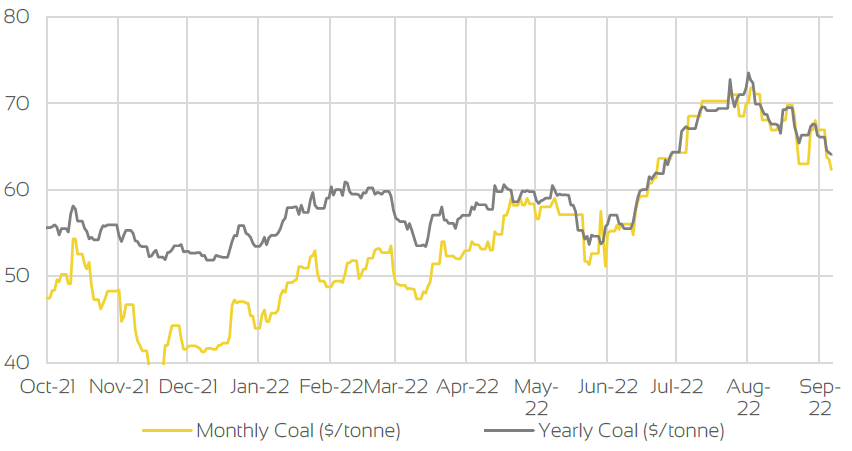

Coal Prices

Market Insight: Long-Term

Seasonal contracts followed a similar trend to prompt contracts throughout August, as prices found support throughout the month as concerns over the certainty of supply continued to be the predominant driver until the last week of the month. During the last week, despite Nord Stream 1 flows being reduce to zero, we saw contracts retrace sharply, after hitting all time peak levels. Similar to prompt contracts, prices found support from reduced Russian flows, as concerns remain over how long gas will flow from Russia into Europe, in addition to tightened global LNG supply, particularly as the uncertainty over the Japanese LNG deal with Russia at Sakhalin, remained.

Early in the month, concerns also remained over storage levels, in particular, Germany, as they announced they did not expect to hit either their own target to have storage 85% full, or the EU's target of 80% full by 1st November. Although strong injections throughout the month mean they too are on course to hit these targets now, this initially provided support for prices. We also saw reduced output of the French nuclear fleet, which was operating ~40% of capacity.

Concern over the reliability of the fleet going into Winter continue to persist, with fears alternate sources of generation will be required to replace this output. However, similar to prompt contracts, strong LNG arrivals, healthy injections into EU storage and the proposed introduction of an EU wide price cap, all weighed on prices during the last week, as we saw significant losses to all contracts.

Market Outlook

As we enter September, the market is delicately placed. Strong LNG arrivals to the UK & North West Europe, the proposed introduction of an EU price cap and curbing of demand, in addition to healthy European storage levels, plus the re-introduction of Rough storage in the UK all provide a positive outlook for prices. However, although gas from Russia has been significantly reduced and Europe's reliance on this is waning, concerns still remain over the certainty of this supply. Nord Stream 1 flows currently remain at zero following the end of scheduled three day maintenance period at the end of August, and flows via Ukraine also remain restricted. Whilst the global LNG picture looks far brighter than it did a month ago, concerns still remain, with more countries turning to LNG and the potential for supply issues, continuing. Particularly in America, with the Freeport LNG facility offline until November at the earliest.

Provided we do not see a significant change to the fundamental drivers, it is possible we will see prices soften even as we approach the Winter period, although risk still remains, particularly if the Winter period is colder than expected. In addition to the Bearish factors mentioned, we may also see a significant drop in demand due to a global recession. As interest rates and inflation continue to rise, it is expected that we will start to see global demand reduce, which in turn, should weigh on prices. For further information, or to discuss options, please get in touch with your Optimised Account Manager, or call the number below to speak to one of our experts.

Download the full insight here:

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.