Energy Market Insight | July 2023

Energy Market Trends: JUNE 2023

Prices remained relatively rangebound throughout July

WHAT IMPACTED ENERGY PRICES IN JULY 2023?

TOP 3 FACTORS AFFECTING ENERGY PRICES

- Major maintenance across Norwegian gas plants ease

- Volatile wind generation adds pressure on gas demand for power

- Oil prices rally across July nearing 3 month highs

WHAT ARE THE SHORT-TERM ENERGY PRICE IMPACTS?

Short-Term ENERGY MARKET TRENDS & INDICATORS

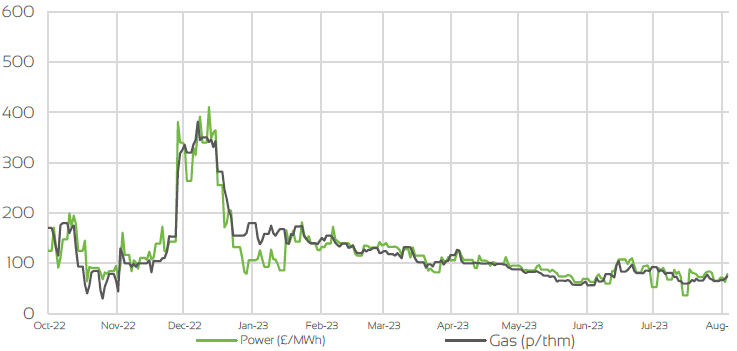

Day Ahead GAS & POWER Prices

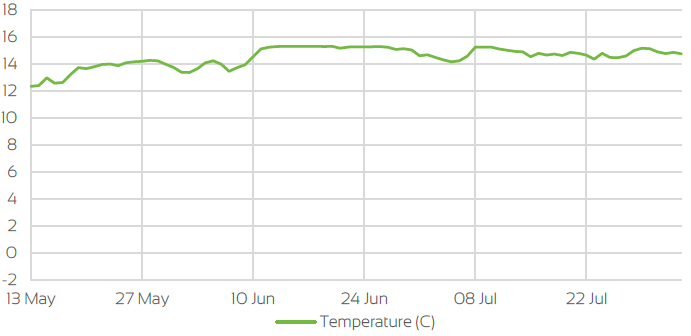

UK Temperature CHANGE

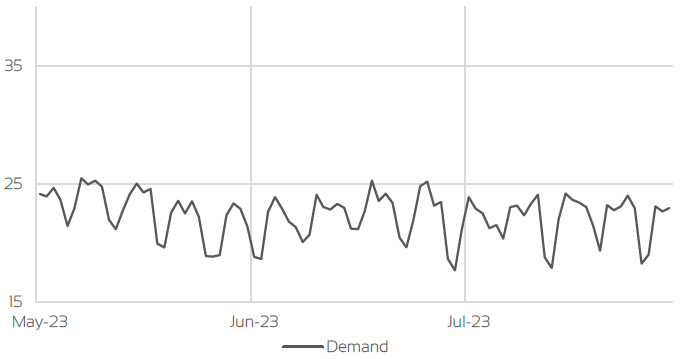

UK Gas Demand - Gigawatt hours (GWh)

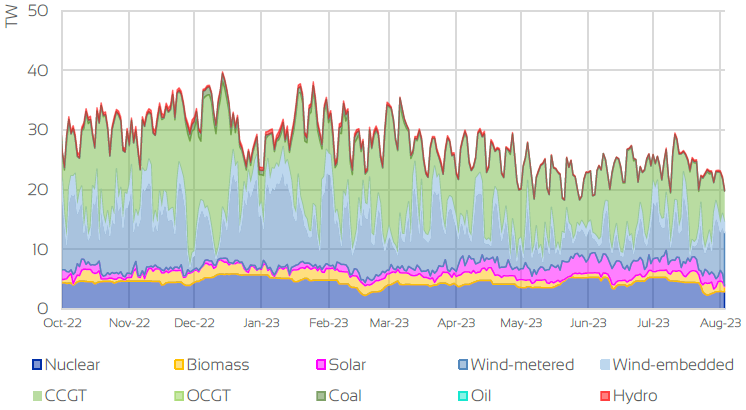

UK GAS SUPPLY MIX

Market Insight: Short-Term

As we now move into the latter part of the summer prices across the prompt markets have remained relatively flat. Monthly index’s across August & September on power sit comfortably under the £80/MWh with gas prompt prices remaining at similar levels as September 23 remains just below the 80p/Therm mark.

Day Ahead prices have remained relatively rangebound throughout July despite Norwegian gas flows increasing towards the end of the month. The increase of gas flows was due to the end of heavy maintenance at selective gas fields across Norway throughout June and July. With that said there are some future planned maintenances scheduled for August which will impact flows during the month but not at the levels we saw during June and July. Maintenance at Troll and Kollsnes start today and will run until 13th (Troll) and 21st (Kollsnes) respectively, alongside works at Oseberg which will start on 3rd and ends on 11th.

LNG cargoes coming into the UK and the EU remained sparce in July due to ongoing maintenance at numerous terminals in the US. This coupled with increased demand in Asia due to warmer temperatures has meant bidding for LNG has become more competitive, and in turn has hindered the numbers of LNG arrivals.

As winter nears, storage levels across the UK and Europe remain extremely healthy and on course to hit current targets to cope with the winter demand. European storage levels were 86% full by the end of July and likely to hit their targets by around the end of September if current injection rates continue. Renewable output again has been inconsistent with generation overall being weak as reduced wind speeds was apparent throughout July, increasing gas demand for power.

WHAT ARE THE LONG-TERM ENERGY PRICE IMPACTS ?

LONG-Term ENERGY MARKET TRENDS & INDICATORS

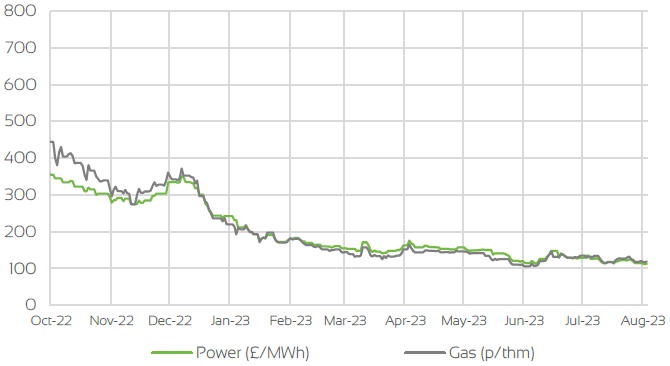

Front Seasonal gas & power Prices

Brent Crude & Carbon Price

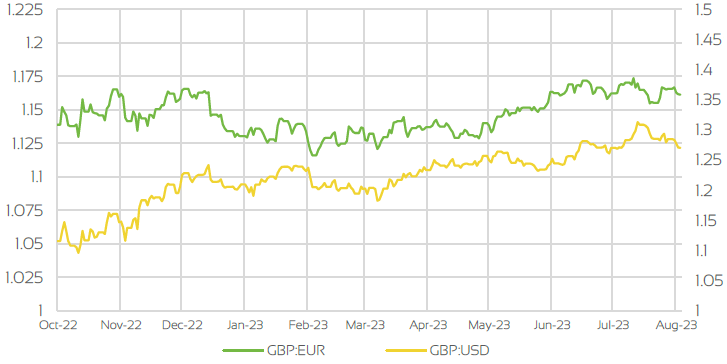

UK, EU & US Currencies

Coal Prices

Market Insight: Long-Term

Seasonal markets have fared in similar vain to prompt contracts throughout July, as extended maintenance has meant winter 23 and Summer 24 index’s have seen some upside but overall, again remained relatively flat throughout the month as prices have generally reversed after some short gains. Markets seem to have adjusted to the risk’s surrounding maintenance, but fears are still persistent as we move closer to the winter months due to the recent lack of LNG despite storage levels across Europe on course to meet their targets.

Heatwaves across Asia generally means cooling demand is likely to increase with bidding on LNG likely to become more competitive, and with LNG ports in the US undergoing maintenance works, added concerns topping up storage level will still remain, coupled with the unknown of how winter temperatures will turn out. Winter forecasts won’t appear until the latter parts of August (at the earliest) leaving seasonal markets relatively sensitive to much of the short-term drivers that effect prompt markets. The Russia/Ukraine conflict still lingers in the background even though markets have adjusted to the risks surrounding the conflict, but the threat of retaliation from Russia if they find evidence of sabotage to Nord Stream 1 is still very much apparent.

Continuing on the wider energy complex, oil prices have rallied throughout July and reached the mid 80’s as the month ended. With economic recovery high on the agenda across the globe, this suggests that demand for oil could increase, impacting demand for power generation and gas. As the winter outlook is unknown at the moment, this is likely to add some upside risk into seasonal contracts.

Market Outlook

As the summer months come and go, we are now considered to be at the latter stages of the summer season. Markets are still considered of being rangebound for the remaining part of the summer and beyond for the time being. As healthy storage levels across the UK & Europe are expected to continue with expectation of targets being met well within the deadlines, fears of supply shortages are eased in the short term. Coupled with expectations on LNG imports improving over the coming weeks, this will only add bearish sentiment into markets.

Though with heatwaves across Europe and Asia and suggestions of further unplanned and unexpected gas outages at some Norwegian gas plants, some of the bearishness is likely to be limited. The UK & Europe compete with Asia for LNG cargo; therefore, the LNG spot market will become increasingly more competitive and potentially impacting the recovery of LNG imports coming into the UK & the EU. The latter part of the summer months also see’s added demand through consumers looking to hedge for the winter period and coupled with the volatility of renewable generation we have been experiencing, this will add further upside pressure into prompts markets, with seasonal contracts also being impacted.

We believe bullishness within the prompt markets will only just supersede the bearish drivers in the latter months of the summer period, as demand for winter hedging increases alongside the volatility of renewable generation and the threat of Asian spot prices for LNG. This will also add risk into seasonal markets, but as we experienced significant downside last winter, there is a case of this being repeated if demand is curbed due to a mild winter alongside storage levels remaining healthy.

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.