September Monthly Market Insight

Supply drivers bring volatility to prompt markets and a weak wider commodity complex pressures the curve.

Market Insight: Long-Term

Movement on far curve contracts has been somewhat less volatile with a weakening commodity complex adding downside pressure to further dated contracts. Oil prices started the month relatively strong as the US dollar weakened, on the Federal Reserve’s announcement of a 2% average inflation target, rather than a flat target. The commodity failed to hold on to gains as coronavirus cases in many of the world’s major economies began to surge once again. Increasing Libyan and Iranian supply also contributed. Even US production being all but stopped, by hurricanes, couldn’t provide support against the bears.

It has been a volatile month for Carbon with anticipation that the EU Commission would announce increases to emissions reductions targets, pushing Carbon above the €30/tCO2e mark. Following the announcement of increased targets to 2030, the market reaction somewhat flopped as the mechanism of the increases, including potential for use of alternate base levels for 1990 and increasing renewable output across Europe, seemed to dampen initial excitement.

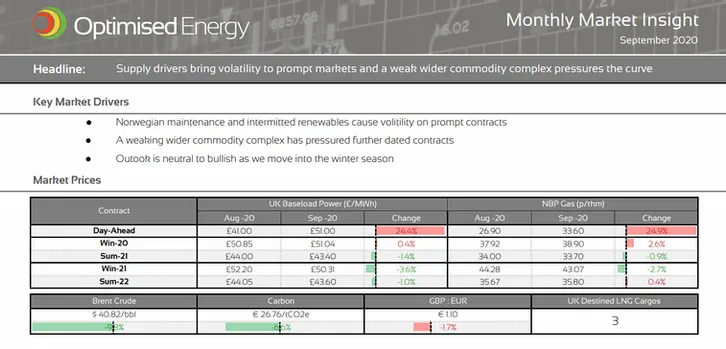

Market Outlook

In the shorter term, the outlook is neutral to bullish with movement being mainly supply/demand driven. Temperatures are expected to sit below seasonal norm until mid-October, increasing demand for heating. Longer-range forecasts hint at a more settled second half to the month. This could create volatility on prompt contracts if renewable generation drops off. Norwegian maintenance is largely complete but there is always potential for unplanned outages. Further ahead, weakening of the wider commodity complex could provide downside, however, progress with the UK/EU trade deal will weigh in. The Pound has seen significant volatility throughout September and pessimism around any deal has the potential to create further downside for the Pound.

Markets have significantly recovered over the month of September. The market contango, seen for much of the summer, is softening and could indicate a period of backwardation is on the horizon. The effect is more pronounced on the power curves with the front 6 winter gas seasons tracking fairly flat to one another. Fixed clients should consider the opportunity backwardation could present for securing volume further ahead. Alternatively, clients should select a longer-term flexible strategy to take advantage of any emerging opportunities to secure volume further ahead.

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.

OUR OFFICES

ASHBY DE LA ZOUCH

1 Ivanhoe Office Park

Ivanhoe Park Way

Ashby de la Zouch

Leicestershire, LE65 2AB

BLACKPOOL

109-112

Lancaster House

Amy Johnson Way

Blackpool, FY4 2RP

BRISTOL

Hanover House

Queen Charlotte Street, Bristol, BS1 4EX

SITTINGBOURNE

The Oast

62 Bell Road

Sittingbourne

Kent, ME10 4HE