Energy Market Insight | January 2025

Energy Market Trends: January 2025

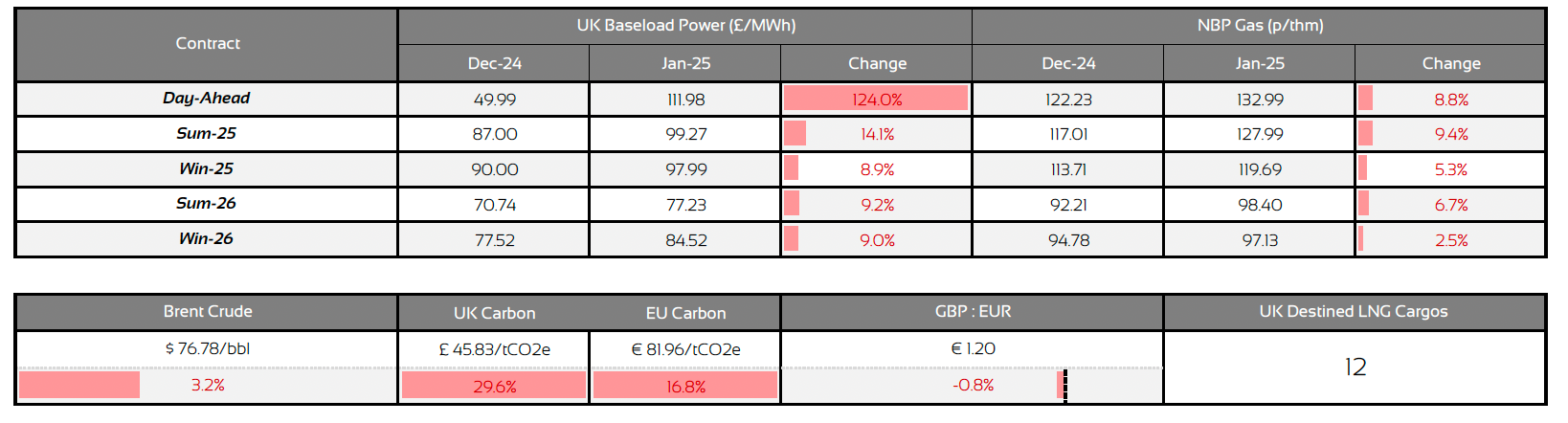

UK Gas and Power contracts remained volatile due to colder weather and continued geopolitical tensions

WHAT IMPACTED ENERGY PRICES IN JANUARY 2025?

TOP 3 FACTORS AFFECTING ENERGY PRICES

- Colder Weather increased demand for gas and depleted storage levels

- Geopolitical tensions across Europe and the Middle East continues to add volatility

- LNG supplies remained strong throughout January, easing some concerns

WHAT ARE THE SHORT-TERM ENERGY PRICE IMPACTS?

Short-Term ENERGY MARKET TRENDS & INDICATORS

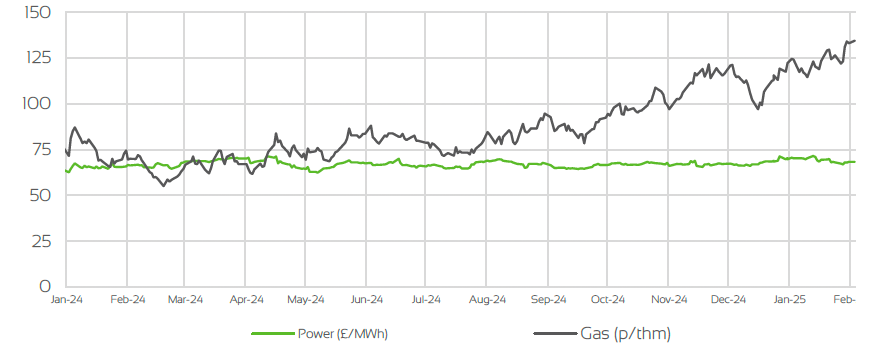

Day Ahead GAS & POWER Prices

UK Temperature CHANGE

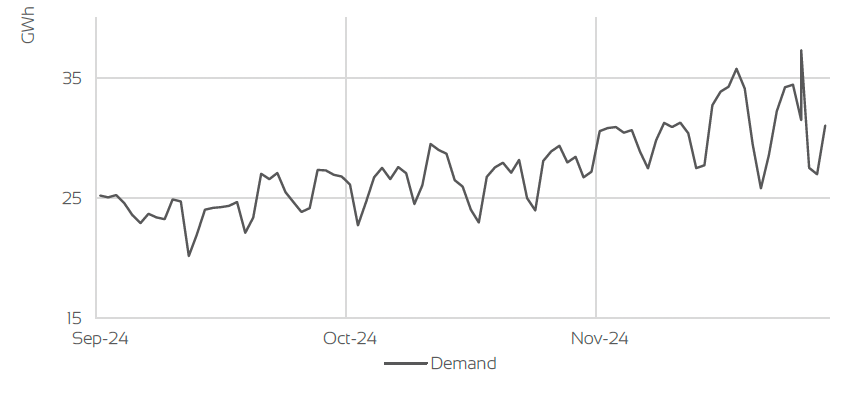

UK Gas Demand - Gigawatt hours (GWh)

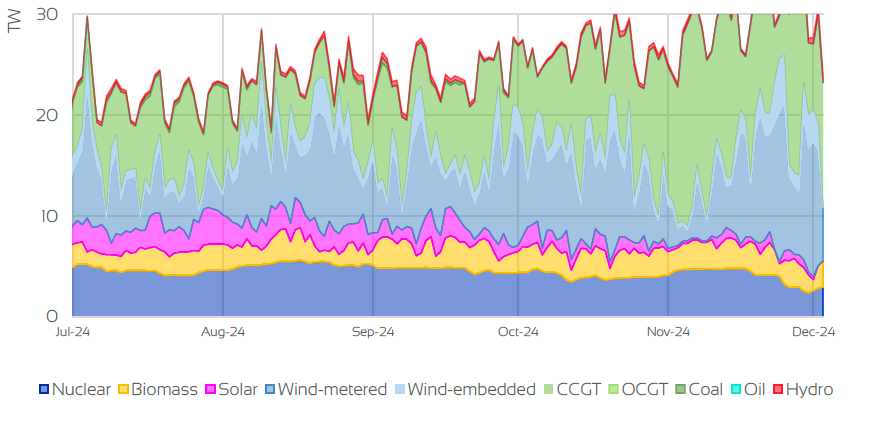

UK GAS SUPPLY MIX

Market Insight: Short-Term

January experienced heightened volatility due to fluctuating weather patterns, geopolitical tensions, and shifting supply dynamics.

Gas demand surged early in the month due to colder-than-seasonal temperatures, but milder forecasts towards mid-January eased some concerns about storage levels, which remained below historical averages at around 65% full.

Norwegian gas flows remained stable despite intermittent maintenance, while robust LNG deliveries supported a comfortable supply outlook. Renewable output fluctuated, contributing to short-term volatility in power prices.

Geopolitical risks, including Ukraine's targeting of critical infrastructure and U.S. sanctions on Russian energy, added bullish sentiment to markets. Meanwhile, Brent crude oil prices hovered between $75 and $81.5/bbl, driven by tight U.S.

inventories, OPEC+ decisions, and supply disruptions from sanctions on Russia and Iran.

Overall, the market balance shifted between bearish and bullish factors, keeping prices sensitive to weather and geopolitical developments.

WHAT ARE THE LONG-TERM ENERGY PRICE IMPACTS ?

LONG-Term ENERGY MARKET TRENDS & INDICATORS

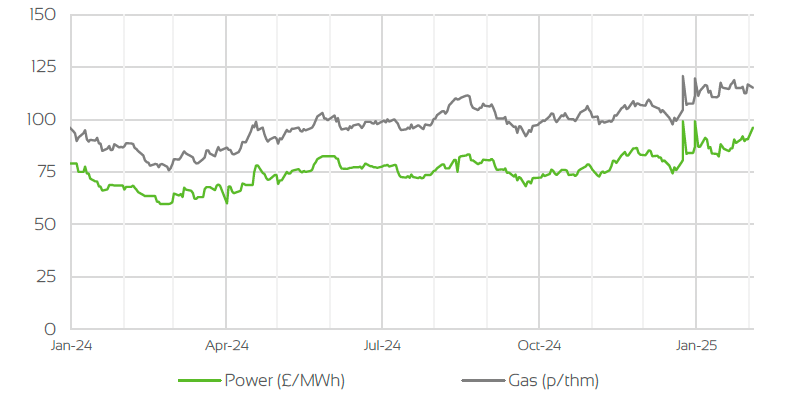

Front Seasonal gas & power Prices

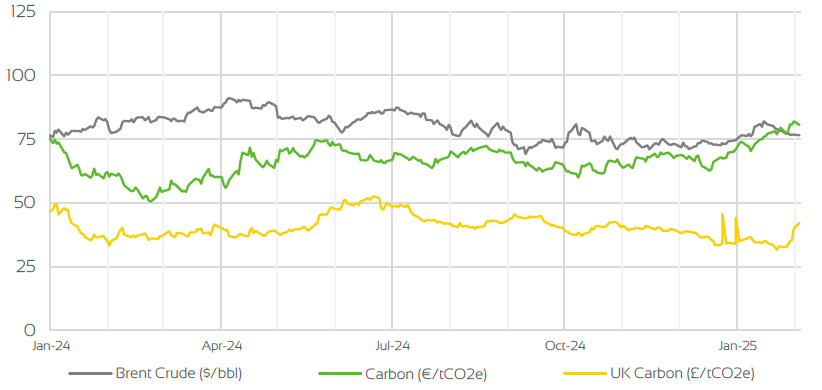

Brent Crude & Carbon Price

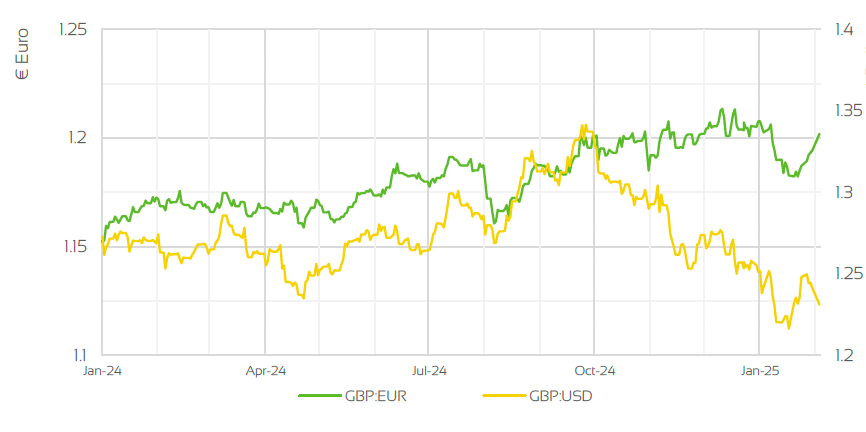

UK, EU & US Currencies

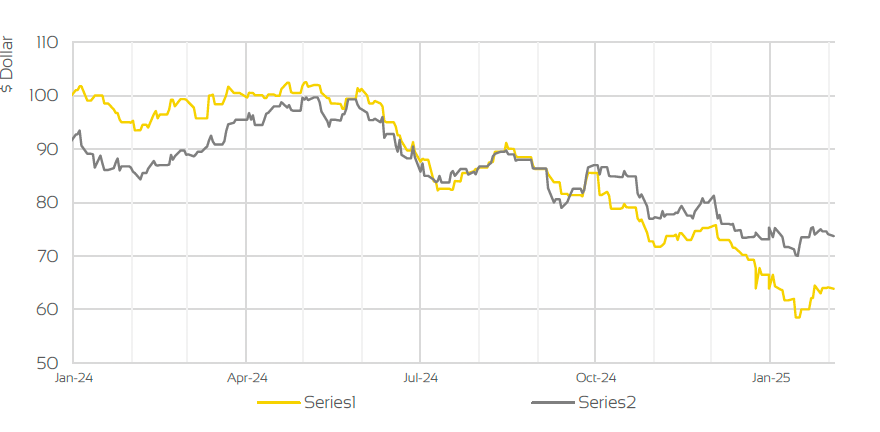

Coal Prices

Market Insight: Long-Term

Looking ahead, UK gas and power prices are expected to remain under pressure as temperatures are forecasted to stay below seasonal norms for the rest of February. The primary focus will continue to be on gas storage reserves, which have been depleting rapidly to meet seasonal demand. Further withdrawals to meet gas consumption will likely exert additional upward pressure on gas contracts.

Although the market has largely shifted its focus away from geopolitical tensions in the Middle East and Eastern Europe, the recent re-entry of Donald Trump into the political arena has introduced renewed volatility, particularly regarding his stance on the Panama Canal and Iran. Norwegian gas flows are expected to remain stable, alongside strong LNG cargo deliveries, which should help limit significant upside potential in gas prices.

Market Outlook

While the landscape appears stable due to healthy supply fundamentals, short-term price volatility is likely to continue due to geopolitical uncertainties and weather variability. Concerns around gas inventories in Northwest Europe and replenishment in the summer will also be a focus and may support further upside come the summer months. US policy toward Iranian oil is expected to add upward pressure on gas contracts, as any action against Iran could prompt the country to block the Strait of Hormuz, a critical passage for the majority of LNG cargoes operators.

The extent of gas withdrawals throughout Q1 2025 will play a significant role in steering price direction. However, stable Norwegian gas flows and consistent LNG imports are expected to provide some degree of price stability. On the wider commodity complex, the UK Government may link UK carbon allowance prices to the EU, although not yet confirmed, this could increase gas and power contracts prices in long term.

Related News

EXPLORE OUR OTHER ENERGY MARKET INSIGHTS

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.

OUR OFFICES

ASHBY DE LA ZOUCH

1 Ivanhoe Office Park

Ivanhoe Park Way

Ashby de la Zouch

Leicestershire, LE65 2AB

BLACKPOOL

109-112

Lancaster House

Amy Johnson Way

Blackpool, FY4 2RP

BRISTOL

Hanover House

Queen Charlotte Street, Bristol, BS1 4EX

SITTINGBOURNE

The Oast

62 Bell Road

Sittingbourne

Kent, ME10 4HE