Energy Market Insight | March 2025

Energy Market Trends: MARCH 2025

Falling demand and steady supply outlook supports losses

WHAT IMPACTED ENERGY PRICES IN MARCH 2025?

TOP 3 FACTORS AFFECTING ENERGY PRICES

- Storage replenishment will remain a key factor

- Muted demand adds bearishness into markets

- Global trade war looms amid U.S tariffs

WHAT ARE THE SHORT-TERM ENERGY PRICE IMPACTS?

Short-Term ENERGY MARKET TRENDS & INDICATORS

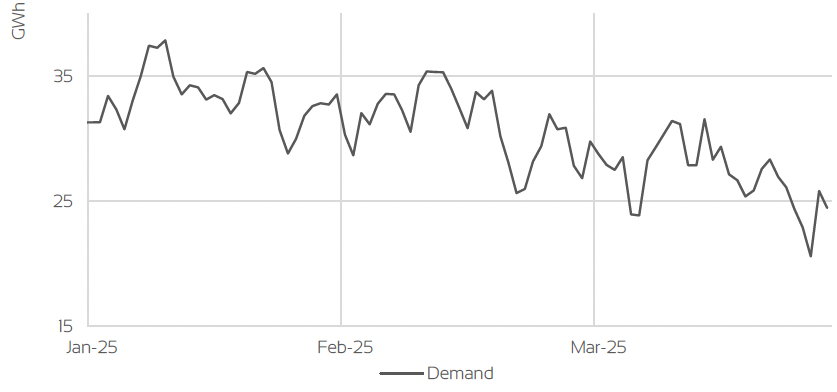

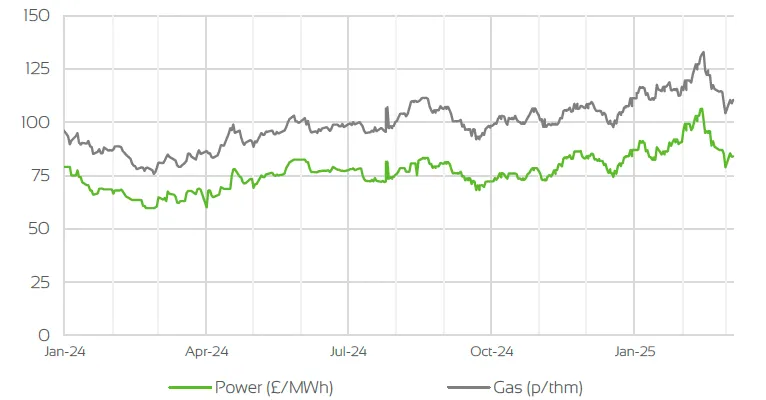

Day Ahead GAS & POWER Prices

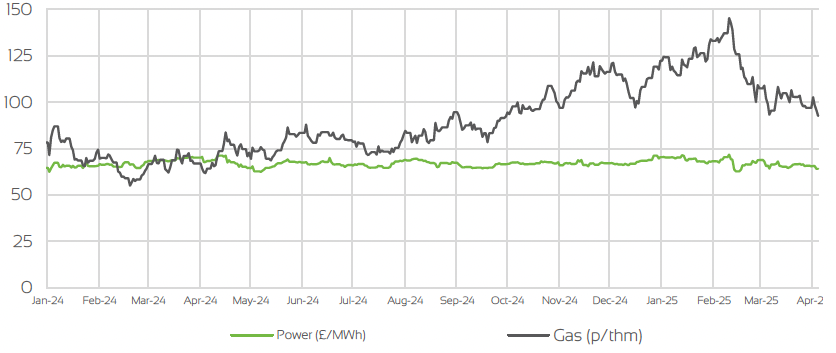

UK Temperature CHANGE

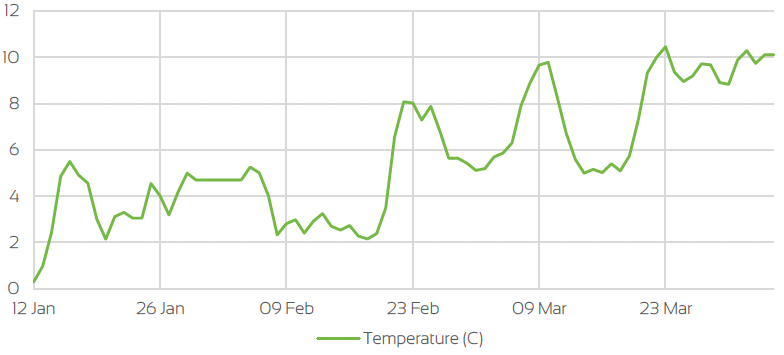

UK Gas Demand - Gigawatt hours (GWh)

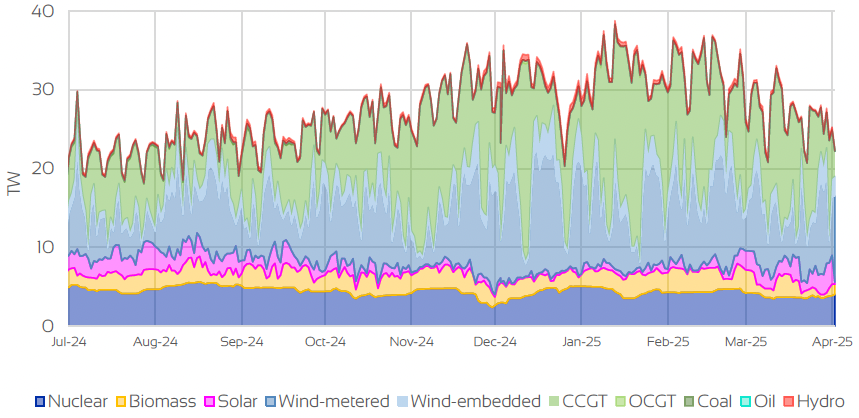

UK GAS SUPPLY MIX

Market Insight: Short-Term

Despite some supply and storage concerns still persisting, markets overall were down by the end of March, as volatility remained somewhat apparent, especially in the early stages of the month. With that said, as March progressed, warmer weather conditions and robust LNG imports and Norwegian gas flows offset storage concerns and the ongoing geopolitical risks that remain.

Trumps new tariff policies also provided some worries around growth and a trade war but has had little impact on prompt gas and power markets for the time-being. As March progressed and the summer months were upon us, temperatures in the UK and Northwest Europe rose and were at norms or above, which in turn lowered demand. This meant LNG send-out (storage injections) were higher and likely to have taken some focus off the current levels of storage which are significantly lower than this time last year and on average over the past few years.

Though concerns around future weather forecasts remained, as any colder spells could prevent stronger replenishment and would mean hitting winter targets (90% by November) could prove challenging. There were talks of reducing such targets to help keep prices steady but were rejected for this year at least. With Trump also pushing for a peace deal between Russian and Ukraine, the short-term outlook could lean towards the bearish side as we approach April and the start of the summer period.

WHAT ARE THE LONG-TERM ENERGY PRICE IMPACTS?

LONG-Term ENERGY MARKET TRENDS & INDICATORS

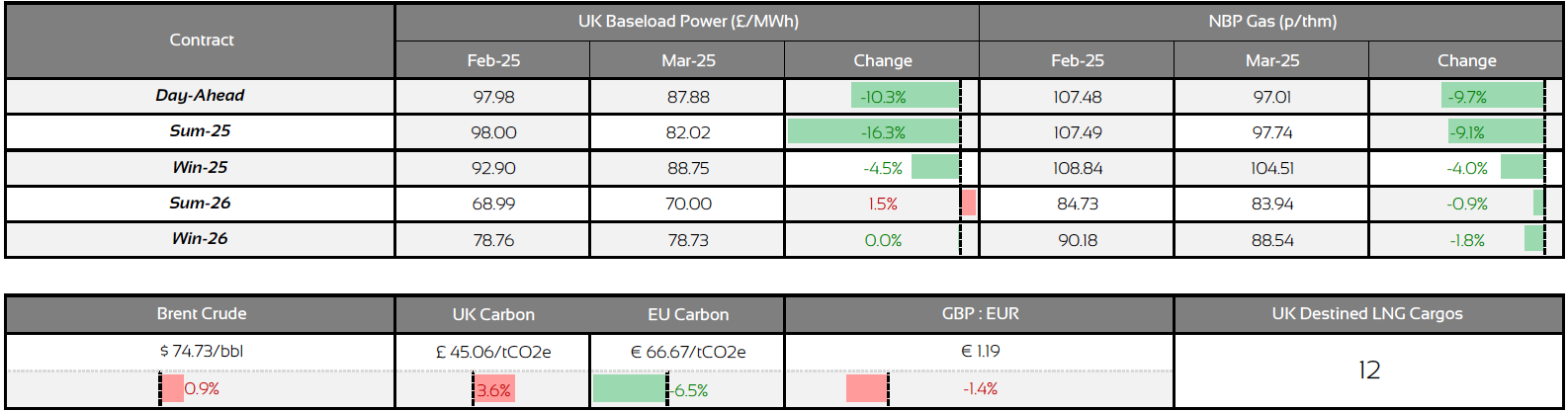

Front Seasonal gas & power Prices

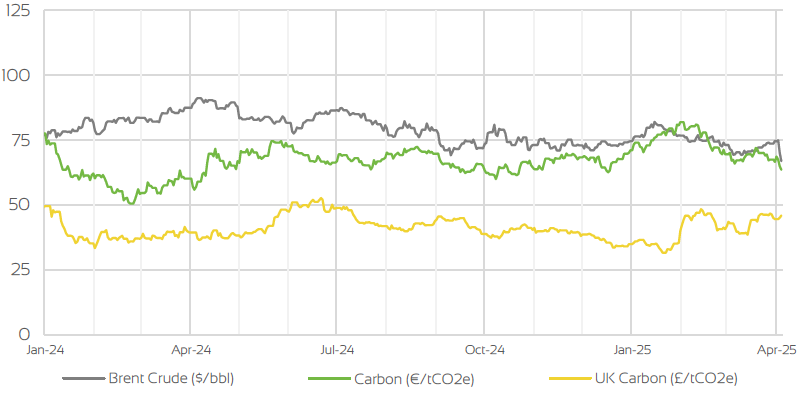

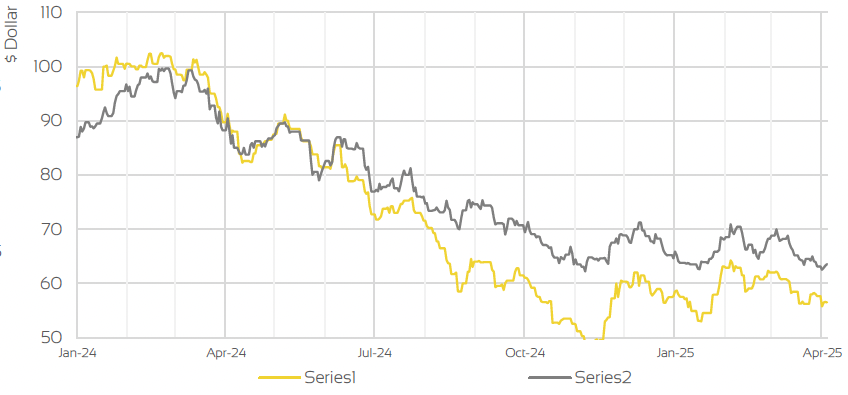

Brent Crude & Carbon Price

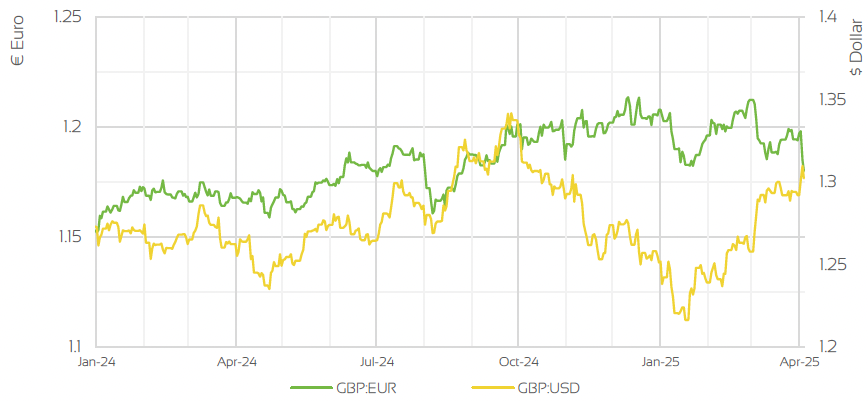

UK, EU & US Currencies

Coal Prices

Market Insight: Long-Term

Seasonal contracts trended bearishly in the second half of March, with summer and winter contracts for 2025 reflecting noteworthy losses in both gas and power indexes. Further out on the commodity complex, oil markets experienced gains overall compared to February, with U.S tariffs continuing to be the main price driver. Concerns over a global trade war were high on the list of outcomes, with risk of supply overall being tighter despite OPEC+ not changing their stance on increasing production in Q2. Though with that said, economic growth could be at risk which can contribute to diminishing demand, leaving the price direction bearish in the longer term. With that said, the impact on UK and European gas & power prices is likely to be limited for the time being, as Europe’s main concerns will be around storage replenishment over the summer period.

Despite calls of a pause to fighting for 30 days between Russian and Ukraine, which was not achieved, an agreement on not targeting energy infrastructure was agreed which eased some concerns around the supply outlook for the future. The progress of the peace deal is likely to be concluded in stages rather than a sudden end, therefore the longer-term outlook is likely to remain uncertain as both supply and demand drivers and geopolitical tensions are likely to keep the market somewhat volatile.

Market Outlook

As the supply and demand outlook remains steady, and geopolitical concerns set to remain apparent in the long term, the market outlook will be uncertain for the time-being, as a view on price direction is still not clear. Warmer temperatures at the moment will continue to add bearish sentiment and assist in storage replenishment over the summer which will be the main focus throughout Q2 & Q3. Scheduled maintenance on gas facilities in Norway (due in April) will also be a key factor in the short-term with any interruptions likely to add upside into prompt contracts at least.

Uncertainty will most likely remain throughout the summer, as geopolitical tensions look far from being resolved despite the best efforts from Donald Trump. New U.S Tariffs will also have an impact on the wider commodity complex as a global trade war and concerns around oil demand and economic growth will continue to persist but is likely to have limited impact on gas and power prices, unless tariffs are put on LNG from the U.S, who export a significant amount to Europe and falling gas demand due to reduced economic activity.

Related News

EXPLORE OUR OTHER ENERGY MARKET INSIGHTS

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.

OUR OFFICES

ASHBY DE LA ZOUCH

1 Ivanhoe Office Park

Ivanhoe Park Way

Ashby de la Zouch

Leicestershire, LE65 2AB

BLACKPOOL

109-112

Lancaster House

Amy Johnson Way

Blackpool, FY4 2RP

BRISTOL

Hanover House

Queen Charlotte Street, Bristol, BS1 4EX

SITTINGBOURNE

The Oast

62 Bell Road

Sittingbourne

Kent, ME10 4HE