Energy Market Insight | July 2024

Energy Market Trends: JULY 2024

Market direction mixed despite Middle Eastern tensions

WHAT IMPACTED ENERGY PRICES IN JULY 2024?

TOP 3 FACTORS AFFECTING ENERGY PRICES

- Middle Eastern concerns re-surface amid fresh attacks

- Poor renewables add some volatility into gas markets

- Oil markets slide amid demand concerns

WHAT ARE THE SHORT-TERM ENERGY PRICE IMPACTS?

Short-Term ENERGY MARKET TRENDS & INDICATORS

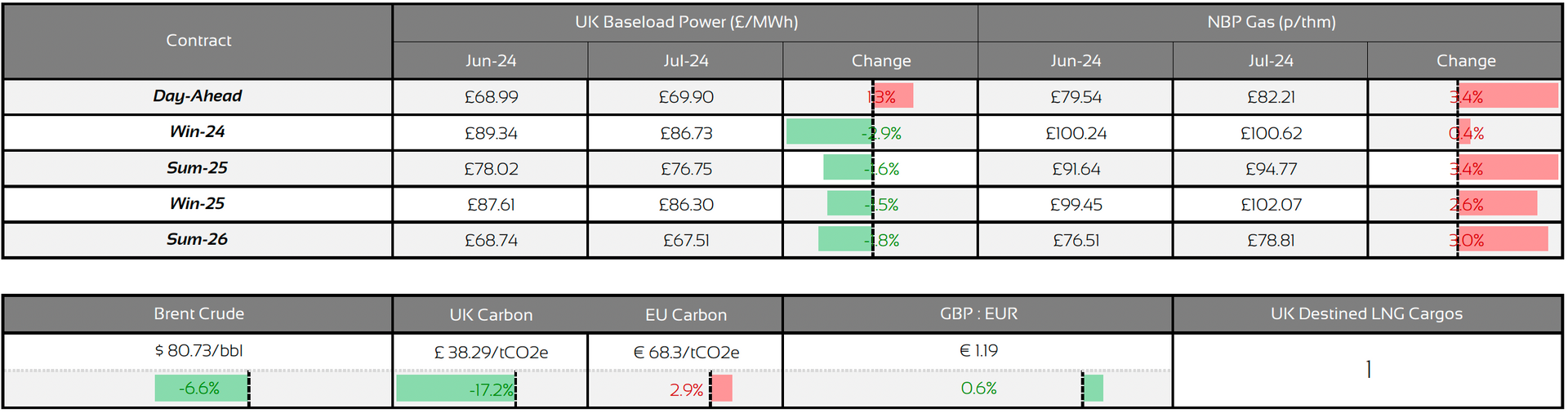

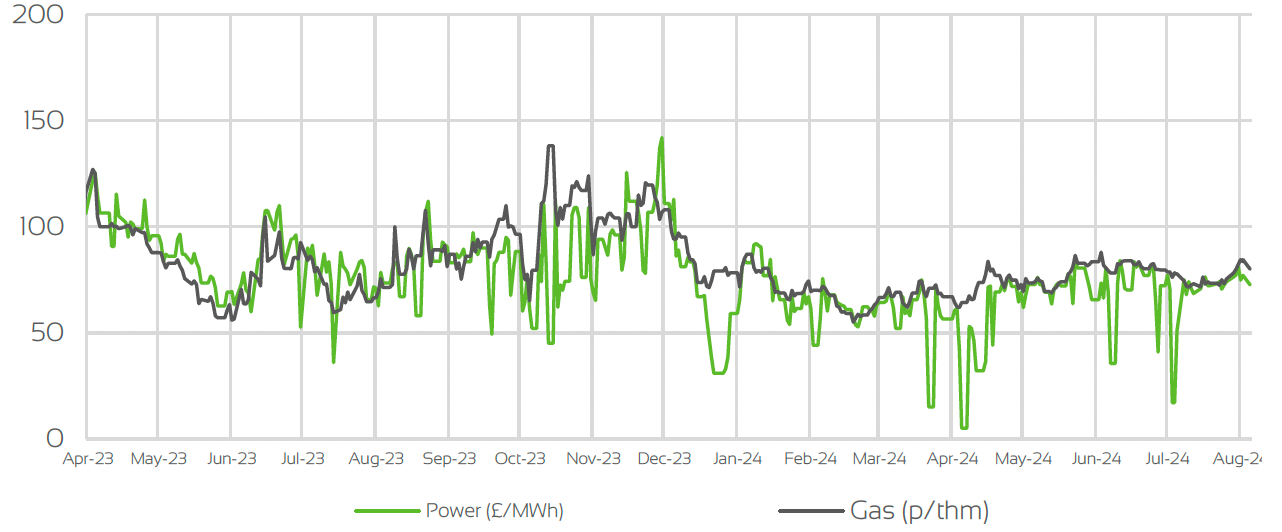

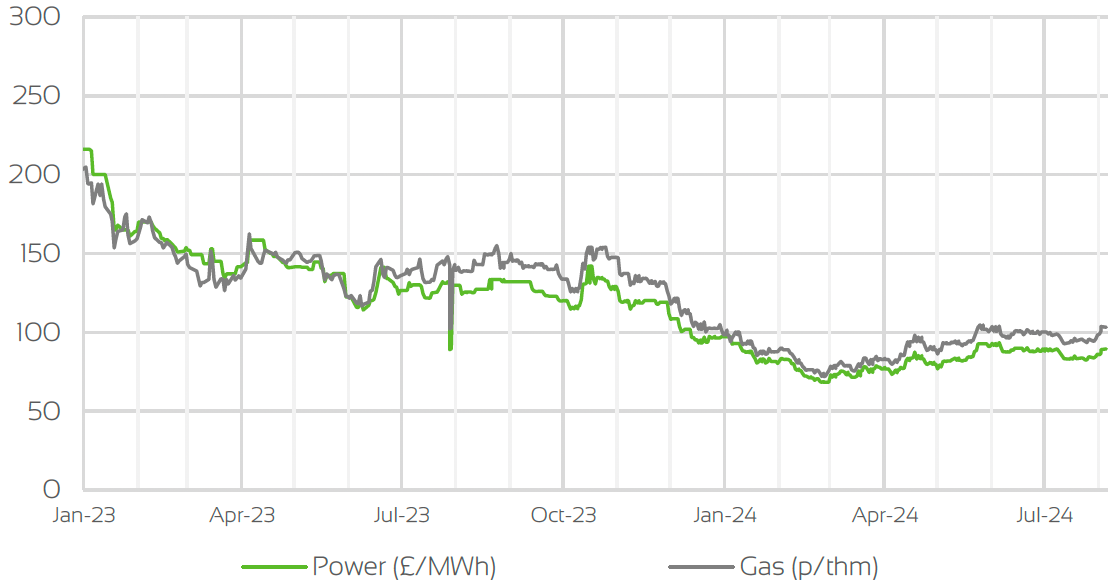

Day Ahead GAS & POWER Prices

UK Temperature CHANGE

UK Gas Demand - Gigawatt hours (GWh)

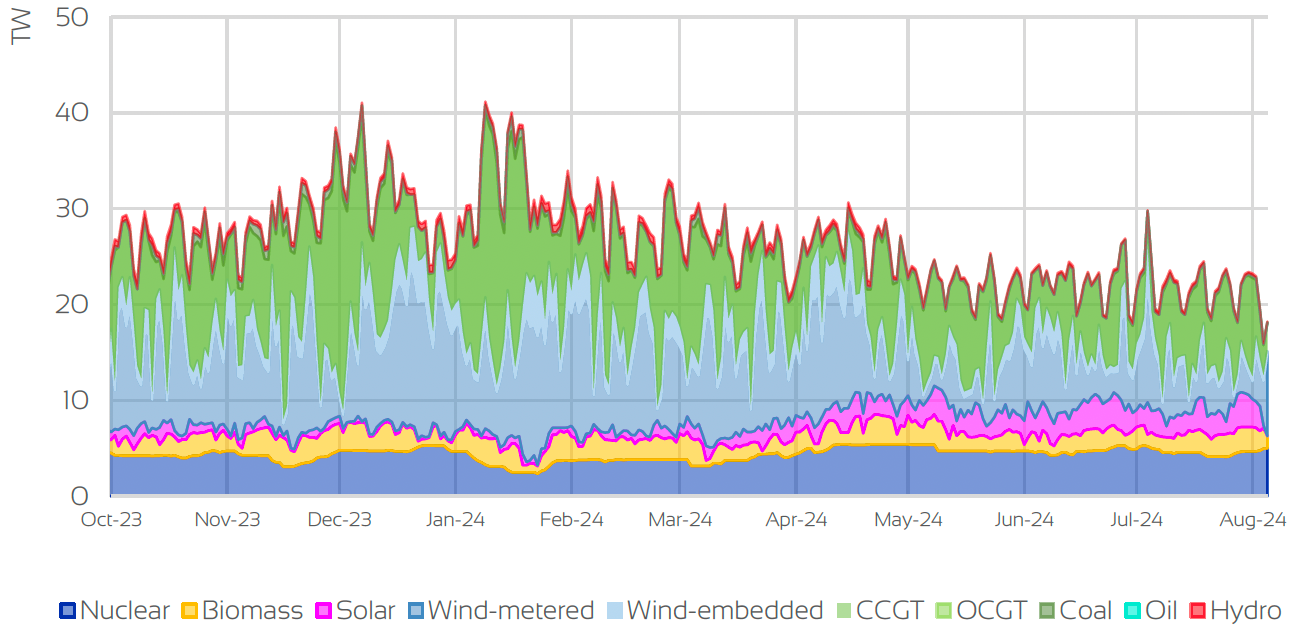

UK GAS SUPPLY MIX

Market Insight: Short-Term

Markets across the curve on both Gas & Power have been mixed overall throughout the month of July. Gas prices across prompt contracts have edged higher overall despite the supply outlook looking largely healthy. Gas storage across Northwest Europe continues to be on a steady incline and on course to be at full capacity by the end of the summer months (target 90% by November).

LNG requirements from Asia is still strong as cooling demand remains high in the region, leaving spot prices for the fuel relatively high. Despite this, LNG sendout (storage injections) remains steady, as reduced demand and strong Norwegian gas flows throughout July kept supplies healthy overall. Outages throughout the month were at a minimum. With that said despite preparations for the winter period seemingly on track, bullishness had crept into markets, as poor wind generation and fresh tensions in the Middle East kept any bearishness in gas prices at bay.

The threat of supply disruptions from the war in Israel, seemed to be easing as ceasefire talks continued, but a fresh attack on Israel territory curbed any hope of an end to the war in the near future. Hezbollah have since denied the latest attack despite blame being placed on them by Israel. This again will stoke fears of the war escalating further into the region, and potentially having an impact on oil and LNG supplies coming from the Middle East.

As gas storage remains extremely healthy, the threat to supply in the short to long term will remain as geopolitical risks continue to add bullish sentiment into markets.

WHAT ARE THE LONG-TERM ENERGY PRICE IMPACTS ?

LONG-Term ENERGY MARKET TRENDS & INDICATORS

Front Seasonal gas & power Prices

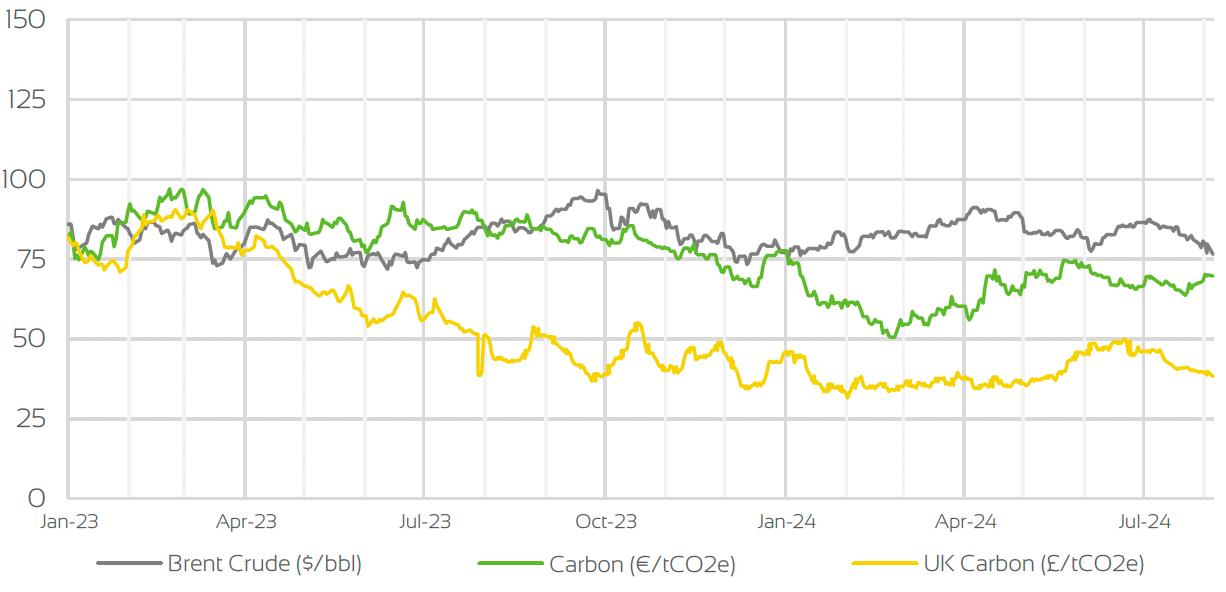

Brent Crude & Carbon Price

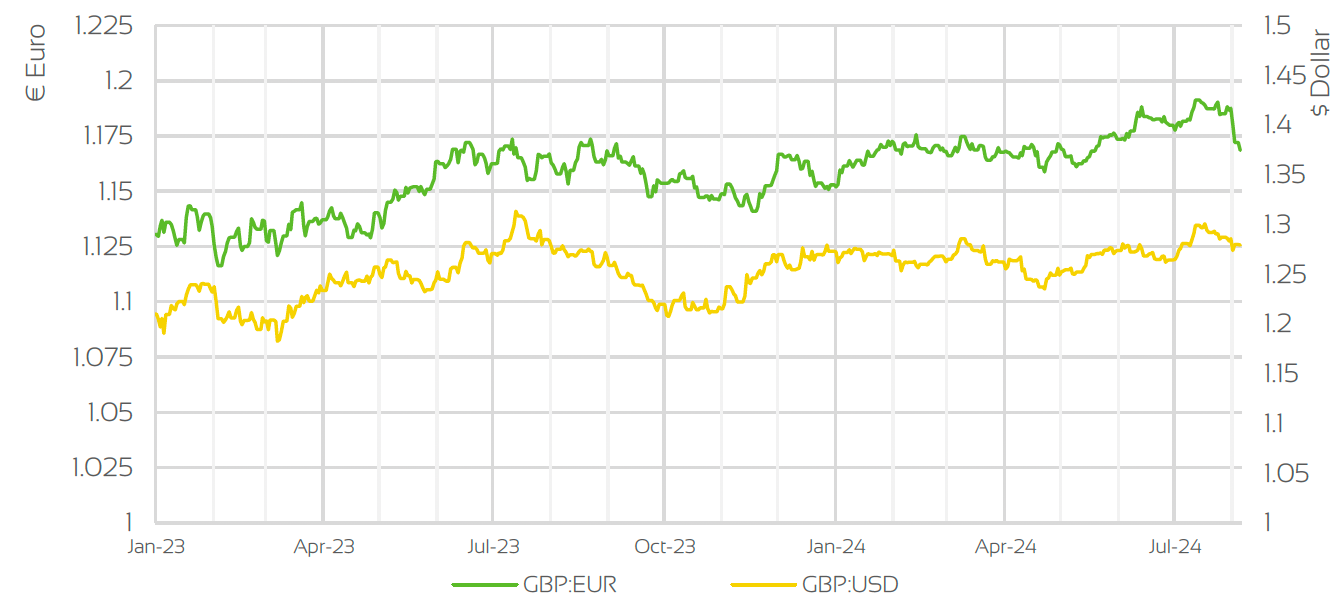

UK, EU & US Currencies

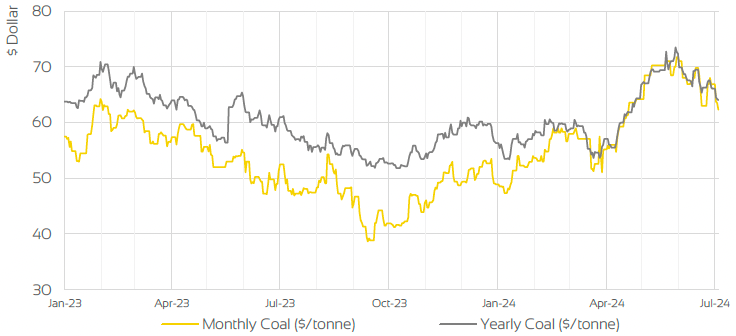

Coal Prices

Market Insight: Long-Term

Markets across seasonal indexes faired in similar fashion to the near curve contracts, as gas prices edges higher, with power prices falling. Overall prices still remained relatively rangebound as contracts continued to trade within a tight range. With the latest concerns coming out of the Middle East and the war in Ukraine still apparent, the risk to the supply outlook will remain somewhat uneasy despite the fundamentals going into the winter months looking strong.

As gas storage levels continued to be at record levels for this time of the year and injections steady, winter-24 and 25 both crept over the 100p/therm mark, as the threat of longer-term disruptions re-surfaced with the latest geopolitical tensions amid the wars in Ukraine & Israel. Muted LNG imports also added bullish sentiment, as the LNG plant in Texas continues to recover from ongoing repairs and the shutdown amid hurricane Beryl. Exports from the region have been muted for a while now, but gas production has steadily resumed, with expectations of exports to ramp up in the coming months, which in turn will ease some of the pressures of higher LNG demand coming from Asia.

On the wider commodity complex, oil prices throughout July have experienced some volatility as demand concerns and summer expectations offset one another. Overall oil prices were down by around 6%, as weak economic data from China, and stronger inventories from the U.S offset concerns from the Middle East and demand expectations from the summer.

Market Outlook

As we approach the latter stages of the summer period, some would suggest markets haven’t quite fallen as expected. With storage levels in Northwest Europe in a very strong position and the general supply outlook relatively healthy, despite some concerns surrounding LNG imports, winter preparations are on course to meet the intended targets with plenty of time to spare. Therefore, there is some optimism that there could be signs of bearishness coming into prompt and far curve contracts. As temperatures are also forecasted to sit above norms in the coming weeks, demand will be reduced adding further bearish sentiments into markets.

With that said the latest concerns from the Middle East and the continued high demand from Asia for LNG will likely push back on any potential losses in the short-term for the time being. Increased demand on the network will also add a premium into prices as winter hedging proves to be stronger at this time of the year. It is likely that markets will continue to trade in a tight range over the coming weeks, as traders will keep a keen eye on developments in the Middle East and the outlook on LNG.

Related News

EXPLORE OUR OTHER ENERGY MARKET INSIGHTS

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.