Energy Market Insight | October 2024

Energy Market Trends: OCTOBER 2024

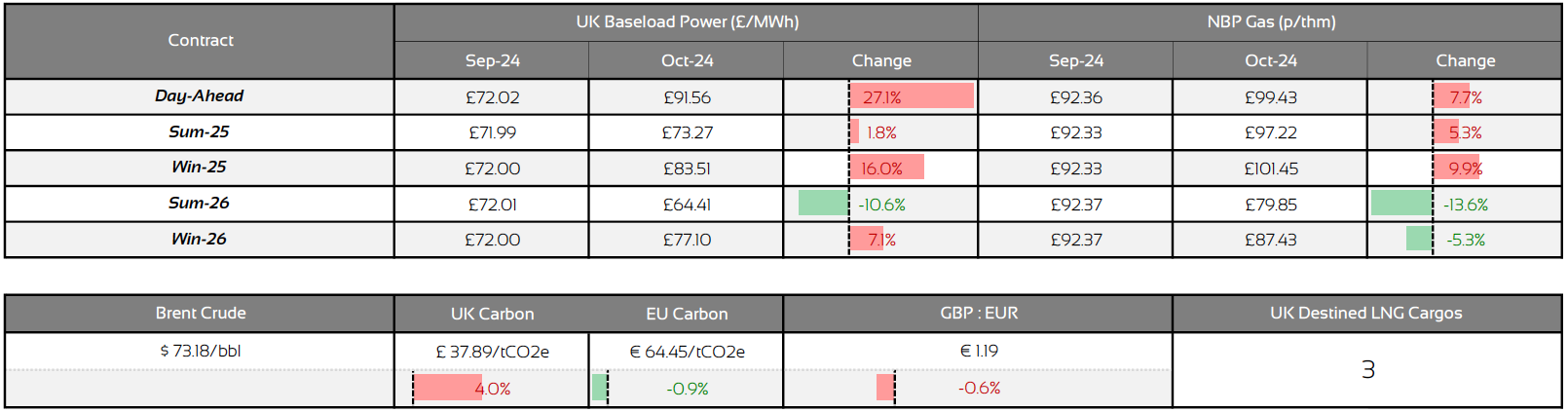

UK NBP gas and power contract prices remained volatile due to fluctuating gas demand and ongoing geopolitical tensions

WHAT IMPACTED ENERGY PRICES IN OCTOBER 2024?

TOP 3 FACTORS AFFECTING ENERGY PRICES

- Continued maintenance in Norway has provided upward support for UK NBP gas prices

- Easing geopolitical tensions and above-average temperatures weigh on prices

- Brent crude oil fell below $70/bbl due to a weak global outlook and an increase in U.S. oil inventories.

WHAT ARE THE SHORT-TERM ENERGY PRICE IMPACTS?

Short-Term ENERGY MARKET TRENDS & INDICATORS

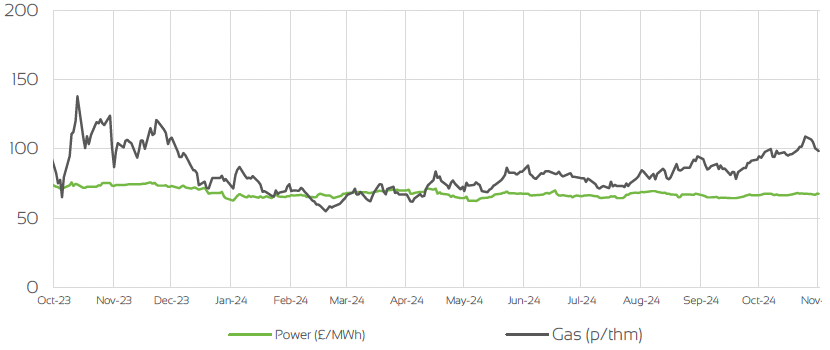

Day Ahead GAS & POWER Prices

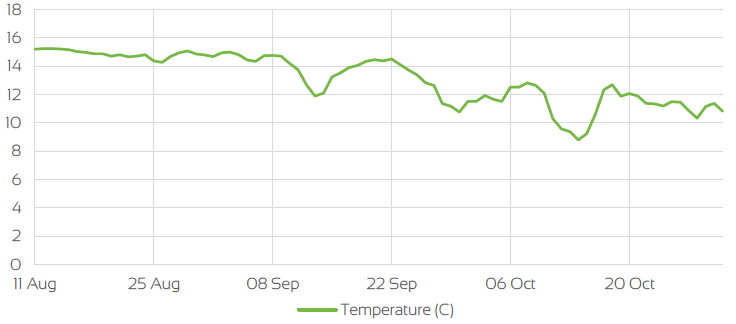

UK Temperature CHANGE

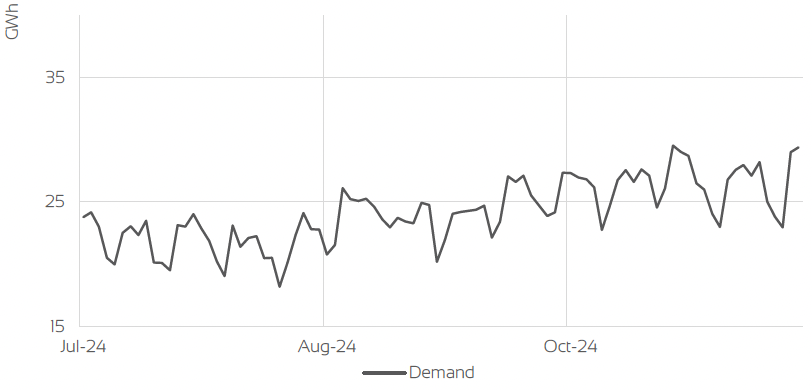

UK Gas Demand - Gigawatt hours (GWh)

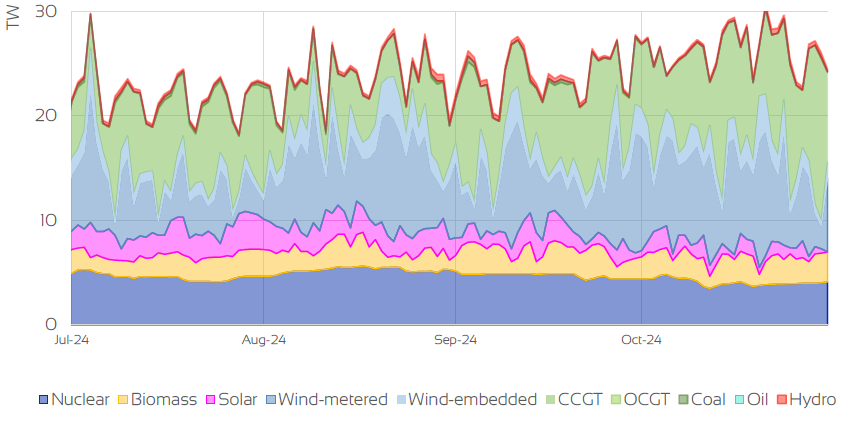

UK GAS SUPPLY MIX

Market Insight: Short-Term

October experienced volatility across UK energy markets, driven by seasonal gas demand, geopolitical tensions, and nuclear outages, which led to an increase in UK NBP day-ahead prices. However, warmer-than-expected temperatures, strong renewable generation, and ample supply conditions limited the upward trend.

Early in the month, mild weather reduced gas demand for heating, while high wind generation helped lower reliance on gas for power, putting downward

pressure on prices. Norwegian supply remained stable despite occasional maintenance disruptions, supporting market stability. Additionally, LNG inflows to the UK remained steady, driven by favourable EU TTF prices.

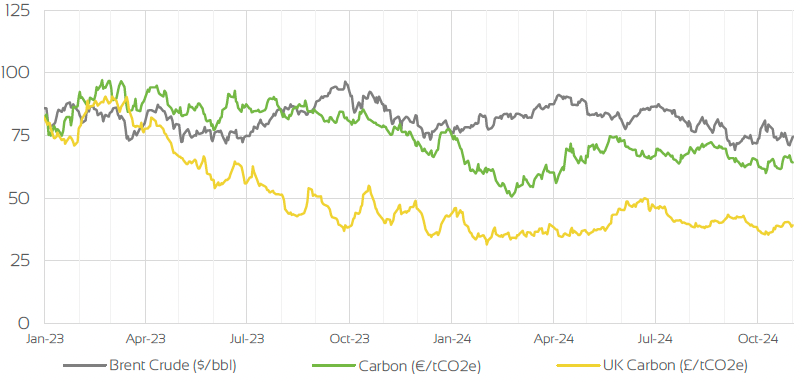

The geopolitical situation in the Middle East added occasional volatility, particularly due to escalations between Israel and Iran. However, prices quickly corrected, as no direct oil infrastructure was impacted, allowing both gas and oil markets to remain relatively steady. By the end of October, oil prices fell close to $70/bbl, weighed down by high U.S. inventories, OPEC+ production increases, and a subdued global economic outlook, despite brief surges driven by Middle Eastern tensions.

WHAT ARE THE LONG-TERM ENERGY PRICE IMPACTS ?

LONG-Term ENERGY MARKET TRENDS & INDICATORS

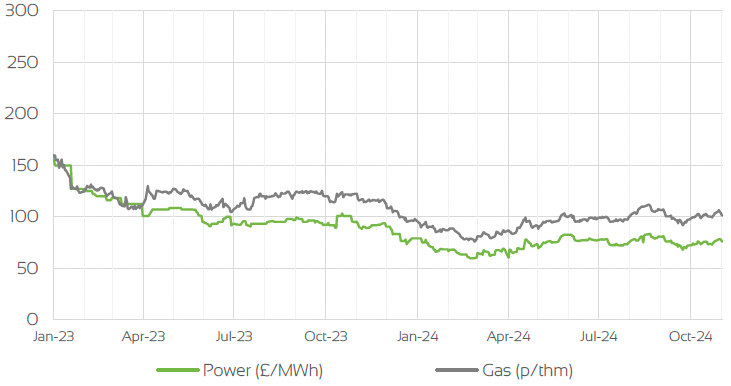

Front Seasonal gas & power Prices

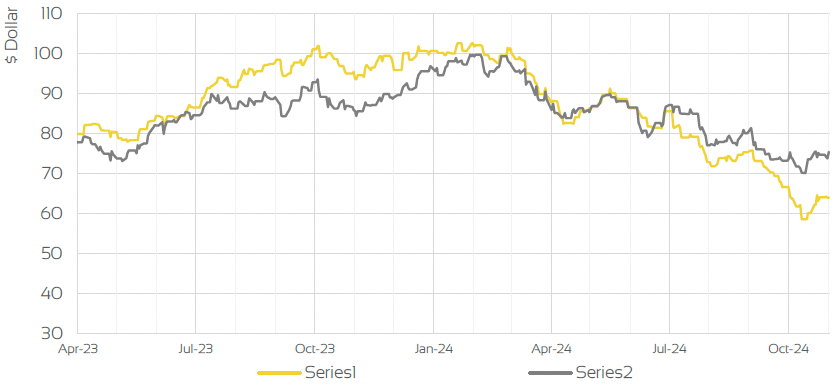

Brent Crude & Carbon Price

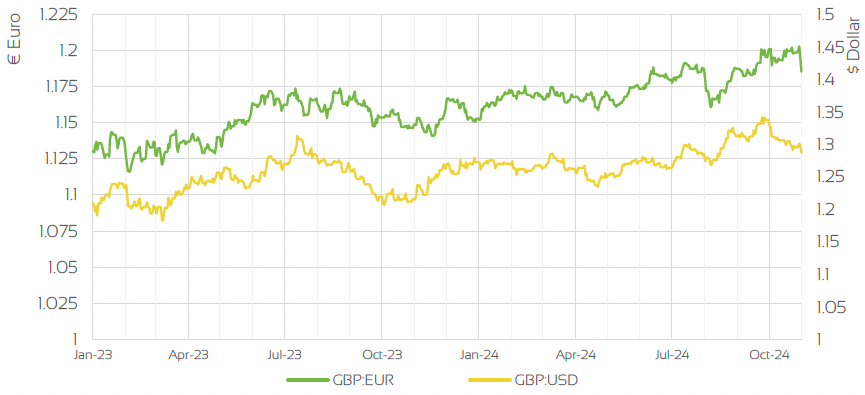

UK, EU & US Currencies

Coal Prices

Market Insight: Long-Term

As we approach the winter heating season, weather patterns and Norwegian gas flows will be pivotal for price stability. October saw mild temperatures, which limited gas demand; however, this is expected to shift as temperatures drop towards seasonal norms in November. Norwegian gas flows should remain stable following the completion of planned maintenance in late October, with stability anticipated to hold through winter barring any unforeseen outages, as no further major maintenance is scheduled until March 2025. While strong storage levels across Europe provide some market resilience, early forecasts indicating colder-than-normal conditions for November could add upward pressure on day-ahead (DA) and Q1-25 UK NBP gas contracts.

Additionally, ongoing geopolitical risks in the Middle East may increase market volatility. Although Israel's recent attack has avoided direct strikes on Iranian nuclear and oil facilities, which has eased geopolitical tension and its impact on LNG routes, but the risk of escalation still remains. With both regional powers now directly attacking each other's territories, a series of retaliatory actions is possible, which could disrupt LNG routes to the EU via the Suez Canal. Moreover, LNG is flowing into the EU due to favourable TTF prices, but competition from Asian economies is likely to increase in the winter months, driving LNG prices higher in the coming months.

Market Outlook

Despite ongoing geopolitical risks in Ukraine and Israel, the overall market outlook remains relatively stable. Gas storage targets have already been met, with current levels at 93%, despite several outages in September. The supply outlook for Winter 2024 looks strong, with stable gas flows from Norway and ample LNG cargoes from U.S. ports. As we move into the winter months, the key factors to monitor will be weather patterns and gas flows from Norway. Price volatility is expected to rise as tensions in the Middle East persist, leading to daily fluctuations. While the long-term outlook remains bearish, driven by robust supply fundamentals, geopolitical uncertainty will be a significant factor in short-term price movements. Looking ahead to the summer months, there is likely to be downward pressure on prices as gas demand typically falls due to higher temperatures. However, potential heatwaves in Central Europe and Asia could create upward pressure on prices during that period.

Related News

EXPLORE OUR OTHER ENERGY MARKET INSIGHTS

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.