Energy Market Insight | May 2024

Energy Market Trends: MAY 2024

May see’s significant gains on both Gas & Power contracts

WHAT IMPACTED ENERGY PRICES IN MAY 2024?

TOP 3 FACTORS AFFECTING ENERGY PRICES

- Competition for LNG continues to raise concerns

- Supply risks add bullishness into market prices

- Oil prices fall amid demand concerns & the lack of interest rate movement

WHAT ARE THE SHORT-TERM ENERGY PRICE IMPACTS?

Short-Term ENERGY MARKET TRENDS & INDICATORS

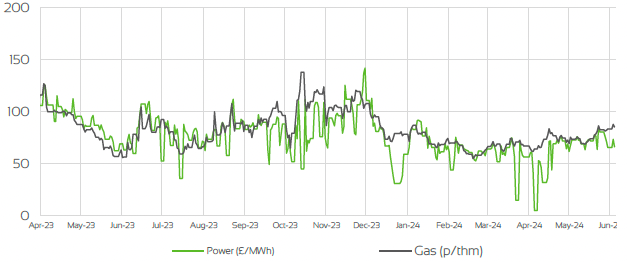

Day Ahead GAS & POWER Prices

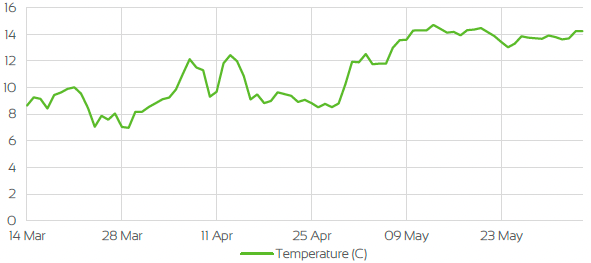

UK Temperature CHANGE

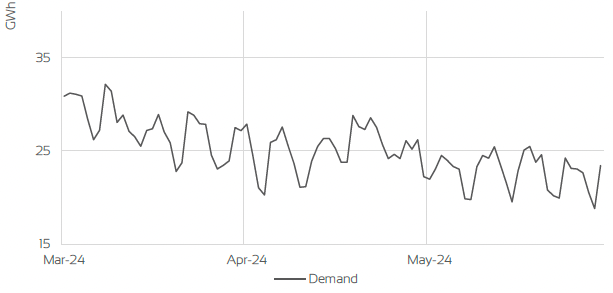

UK Gas Demand - Gigawatt hours (GWh)

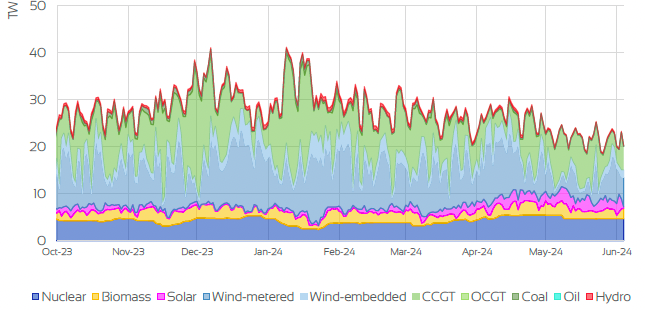

UK GAS SUPPLY MIX

Market Insight: Short-Term

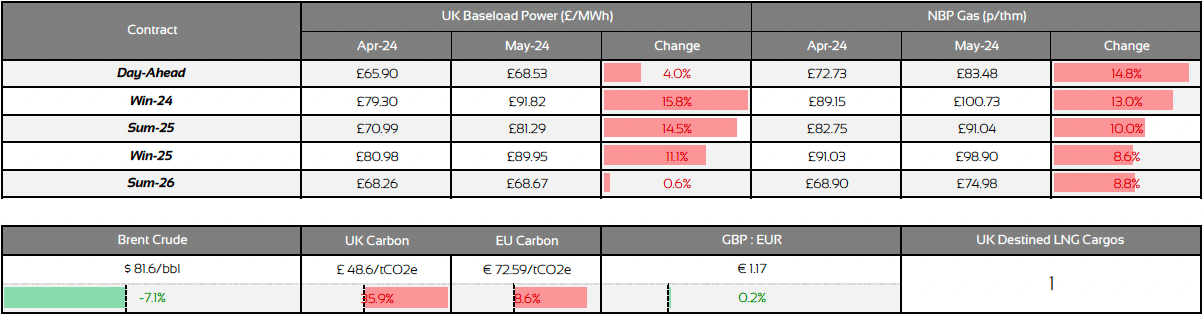

Markets in May have continued in the same vein as April, but the gains have been stronger overall, as fundamental supply risks offset the comfortable supply picture. June, July and August index’s have risen significantly over the month on both power and gas contracts. Gas prices across the near curve are now close to 90p/therm along with power closing in on the £80/MWh mark.

Despite the warmer weather conditions which in turn curbs demand and provides further assistance into storage injections, Norwegian outages have been prominent throughout the month, with large scheduled maintenance works ongoing, albeit for a few days. With that said, smaller outages were also apparent throughout the month, coupled with concerns around LNG exports coming into the UK & the continent, which also supported this month’s bullishness.

A heat wave in Asia meant the demand for LNG had risen, which in turn raises the spot price for the fuel and therefore competition for it increases. Europe have consequently seen shipments reduced compared to previous months, as cooling demand continues to rise in Asia. The Freeport facility which had showed signs of recovery due to increased gas production also remained relatively muted.

Despite the current risks with supply, the outlook remained comfortable as storage in Northwest Europe sat at record highs for this time of the year and was close to 70% fullness at the end of the month, and look set to hit their target of being 90% fullness by November. Wind generation remained relatively steady for the majority of the month and sat around seasonal norms, which in turn kept gas demand for power at bay and looks set to stay that way as we enter into June.

As the wider geopolitical concerns still persist, much of the premiums associated have been somewhat limited in May but will still pose a risk in the short and longer term, as there are no signs of a ceasefire.

WHAT ARE THE LONG-TERM ENERGY PRICE IMPACTS ?

LONG-Term ENERGY MARKET TRENDS & INDICATORS

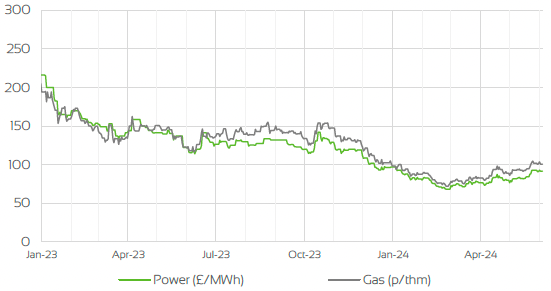

Front Seasonal gas & power Prices

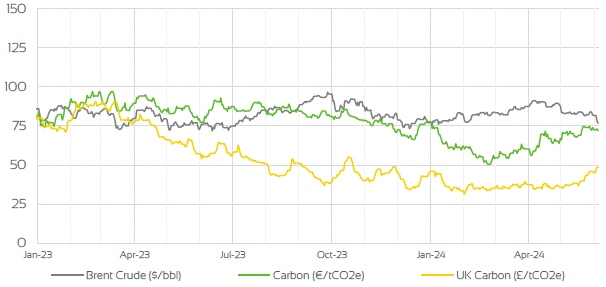

Brent Crude & Carbon Price

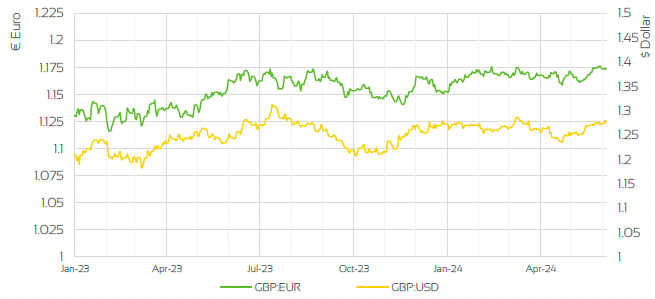

UK, EU & US Currencies

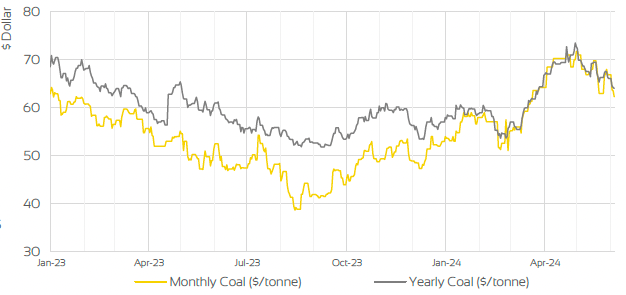

Coal Prices

Market Insight: Long-Term

Contracts along the far curve have faired in the same way as near curve prices and have seen significant gains throughout May, as risks in regards to the supply fundamentals add some concerns of longer term disruptions. The supply outlook overall remains relatively comfortable, with storage levels in Northwest Europe being ample for this time of the year. One of the main concerns that continue to persist and is currently being exacerbated by the increased demand from Asia, is the increased competition for LNG amid the current heatwave, which in turn pushes up the spot price for the fuel as bidding intensifies.

Coupled with the slow recovery of exports from the Freeport facility in the U.S, this has also continued to add bullish sentiment into longer term contracts. Wider risks coming from the everlasting geopolitical tensions in Ukraine and the Middle East still pose a significant threat to the longer term outlook despite much of the premiums looking to have already been priced into markets further out for the time being. With that said any further escalations are likely to add additional gains into contracts depending on the view on how supply will be impacted.

On the wider complex, oil prices have been on the decline throughout May, as demand from the world’s largest users stutter and interest rates in the U.S seem to be static and are not likely to come down in the near future. OPEC+ were due to have a meeting on the 2nd of June to discuss further production cuts, which will give some indication on the direction of oil prices over the next 6 months.

Market Outlook

As we move deeper into the summer months, early signs at the beginning of April suggested that there was still room for further downside, considering the warmer temperature forecasts, ample storage, stable LNG and healthy Norwegian gas flows. We have since seen a steady rise in markets as risks to certain fundamental drivers and wider geopolitical concerns have added much of the upside despite a healthy outlook on the supply picture overall. With the outlook relatively healthy despite some ongoing maintenance works in Norway and heavy competition for LNG exports, if these factors were to remain consistent, there could be room for further gains in the short-term.

Though with no immediate threat to storage injections, renewable generation, and the stable supply of gas from Norway, much of those gains are likely to be limited. Therefore, we could see markets settle and stay relatively rangebound in the short-term at least, but if demand from Asia for LNG was to lose traction and supply from the Freeport LNG facility recovering significantly, there is scope for bearish sentiment to come back into the near and far curves.

Related News

EXPLORE OUR OTHER ENERGY MARKET INSIGHTS

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.